How To Read Financial Reports

Responsibility for an organization’s financial reporting is shared by management, the board and an external auditor.

Financial reports, usually produced on a regularly scheduled basis, provide the opportunity for both management and board members to review an organization’s financial position.

Responsibility for an organization’s financial reporting is shared by management, the board and an external auditor. Management is responsible for preparing financial reports and developing internal financial controls; the board is responsible for overseeing management’s financial reporting processes and ensuring reporting exists to satisfy itself and external stakeholders; and the auditor is responsible for making an independent assessment of the financial statements and giving a professional opinion on whether they give a fair representation of the organization’s financial position.

Both management and the board should be reviewing financials on a regular basis. Management should create an environment where the board can ask enough questions.

While all three have different responsibilities in the process, board members may have the least experience in analyzing financial reporting. While not every financial report is set up exactly the same, there are some key statements board members should be familiar with, and questions they can ask to clarify their understanding an organization’s financial health.

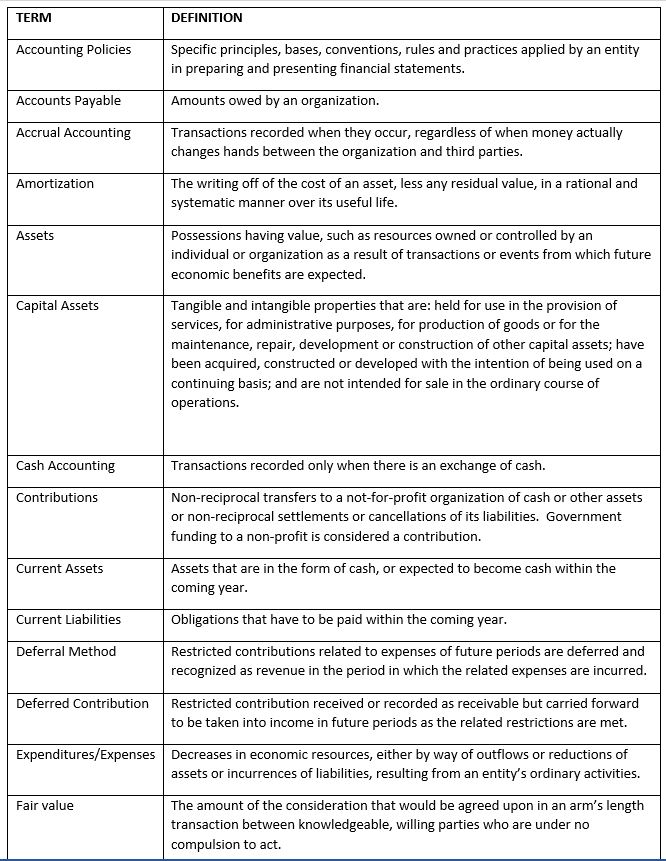

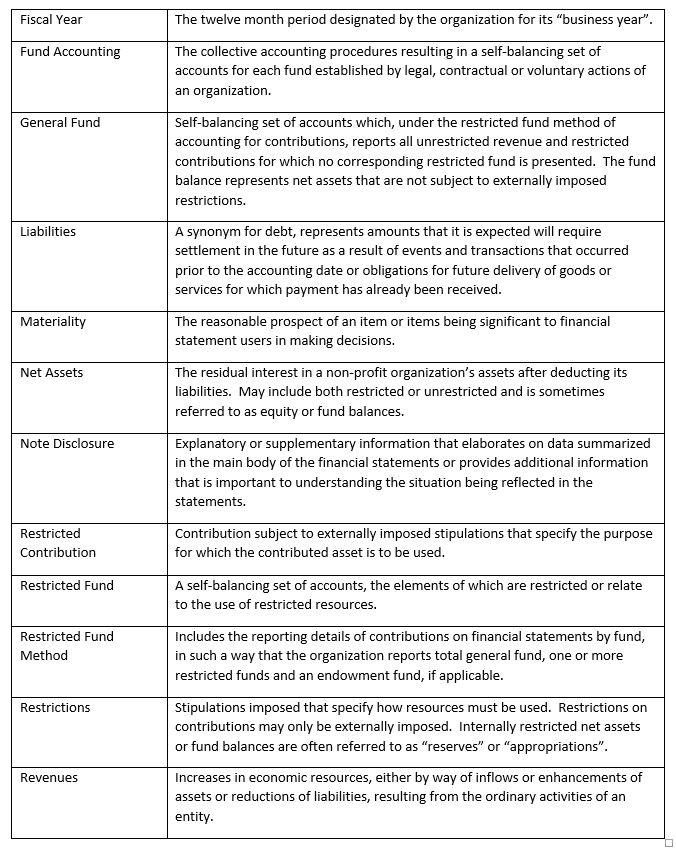

The glossary of terms used in accounting that board members should know includes concepts such as assets, liabilities, revenues, expenditures, accounts receivable, accounts payable, net assets, net revenue, contributions, working capital, etc.

All reporting is based on a time frame, which is different for different reports. Keep in mind, there is a difference between figures presented “at a point in time” — those figures calculated on a particular date, such as assets, liabilities and net assets — and figures presented as “cumulative sums over time,” which refer to the total financial value of an activity during a fixed period of time, such as revenues and expenditures.

According to the Chartered Professional Accountants of Canada, there are two key financial statements board members should review on a regular basis as part of the budgeting process, monitoring of results, or review of the auditor’s financial statements: the Statement of Operations and the Statement of Financial Position.

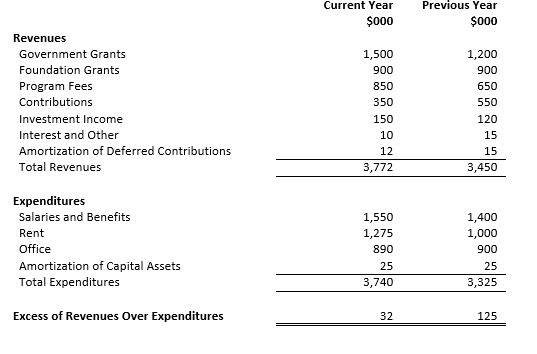

The Statement of Operations, or income statement, summarizes revenues and expenditures over a period of time. It also shows the net balance (in excess or deficit) of revenues over expenditures.

Revenues are the source of funds coming into the organization. Expenditures are the costs of doing business of the organization. Revenues and expenditures are organized in various categories (determined by the organization) usually ranked from largest to smallest.

Non-profit organizations are expected to spend whatever revenues are generated on program delivery — they are not expected to have a profit. However, a small operating surplus, intended to serve as a buffer against unforeseen eventualities, is not unreasonable.

Example of Statement of Operations

Clarifying Questions for Board Members to Ask

The first thing board members should do is compare the figures for the current year to the previous year. There may be changes over time that raise questions. The Chartered Professional Accountants of Canada (2012), recommends some additional questions when considering revenues and expenditures:

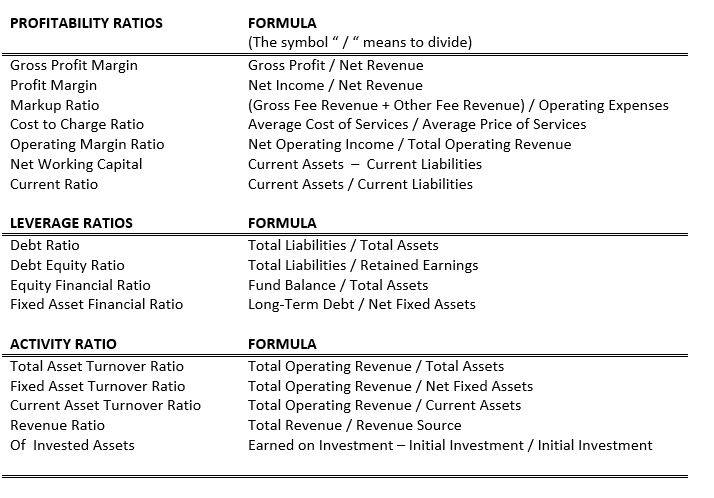

When reviewing the Statement of Operations, board members may use some formulas from the following chart for calculating changes from year to year — in particular, the formula for PERCENTAGE TOTAL REVENUES OVER REVENUE SOURCE.

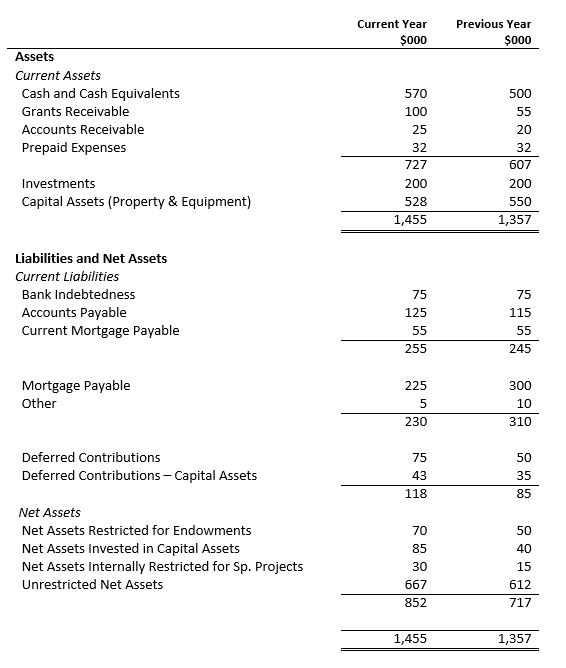

The Statement of Financial Position, sometimes called a Balance Sheet, demonstrates the organization’s financial position at a particular point in time. This report shows how the Total Assets equal the Sum of Total Liabilities and Net Assets.

The Statement of Financial Position organizes assets and liabilities based on how close each is to cash.

• Current Assets – available or easily available cash

• Current Liabilities – need to be paid in current year

• Long Term or “Fixed” Assets – not expected to become cash until future year

• Long-Term Liabilities – not expected to require payment within the next year

Most organizations will normally have more assets than liabilities. What is left over is shown as the balance or Net Assets, which is the net worth of the organization.

Example of Statement of Financial Position

Organization Name

As of December 31, 20XX

Clarifying Questions for Board Members to Ask

Once again, board members should begin by comparing the figures for the current year, compared to the previous year in the Statement of Financial Position. The Chartered Professional Accountants of Canada (2012), also recommends some additional questions:

When reviewing the Statement of Financial Position, board members may use some formulas from the previous chart for calculating changes from year to year — in particular, the formulas for WORKING CAPITAL RATIO, PERCENTAGE CHANGE OF INVESTED ASSETS and PERCENTAGE CHANGE IN CAPITAL ASSETS.

The Statement of Operations and the Statement of Financial Position are linked. The investment income shown on the Statement of Operations is linked to the size of return on investment assets shown in the Statement of Financial Position.

Depending on the area of interest, there are other financial reports that provide useful information about the organization’s finances.

The Statement of Cash Flows shows an organization’s generation and use of cash over a specified time period. It is made up of cash receipts and payments that arise from business set up by principal categories and uses.

Notes to financial statements are additional information provided with the organization’s financial statements, which include: income statement, balance sheet and statement of cash flows. These notes are important disclosures that further explain the numbers in the financial reporting.

Both management and the board should be reviewing financials on a regular basis. Management should create an environment where the board can ask enough questions. All board members should feel comfortable enough to ask questions as needed. However, it is important that questions are answered and then quickly returned to the board level to assess the issue from the strategic level.

Many boards develop a set of dashboard indicators that can be updated by management. When reviewed on a regular basis, these indicators help focus monitoring efforts.